Misspecification of Regression Models

Regression Models

Let’s consider the following regression model:

\begin{equation} \tag{1} \label{eq:linear} y_t = \beta_1 + \beta_2 X_t + u_t \end{equation}

A typical assumption of the linear regression model in \eqref{eq:linear} is that the error term $u_t$ is not related to any independent variables (IVs), i.e., $E(u_t | X_t) = 0$.

However, suppose your specified regression model in equation \eqref{eq:linear} is in fact

\begin{equation} \tag{2} \label{eq:linear_x2} y_t = \beta_1 + \beta_2 X_t + \beta_3 X_t^2 + v_t \end{equation}

Then, the error term $u_t$ in equation \eqref{eq:linear} would become:

$$u_t = \beta_3 X_t^2 + v_t$$

and $E(u_t | X_t) = \beta_3 X_t ^2 \neq 0$.

Visualize it!

Suppose the equation \eqref{eq:linear} is the true model, and the TRYE model is:

$$ y = 1.0 + 1.5 X + v $$

and you estimate it using OLS. Your estimated results are unbiased.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

import numpy as np

# params for noise

mu = 0

sigma = 1

nobs = 50

# Suppose X is has a range 1 to 100 and v is the random noise

X = np.linspace(1,100,nobs)

v = np.random.normal(mu, sigma, nobs)

# Let b1 and b2 be 1 and 1.5 respectively

b1 = 1.0

b2 = 1.5

#y = b1 + b2 * X + b3 * X **2 + v

y = b1 + b2 * X + v

After gnerated $y$, let’s estimate the parameters using OLS.

1

2

3

4

5

6

7

8

9

10

import statsmodels.api as sm

#add constant

Xt = sm.add_constant(X)

#fit linear regression model

model = sm.OLS(y, Xt).fit()

print(model.params)

The estimated results are [0.97627477 1.49862051], which are very close to the true values of 1.0 and 1.5. Not bad, huh?

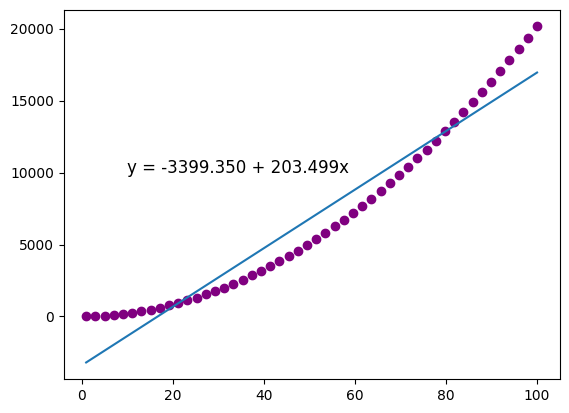

However, what if the underlying TRUE model is $ y = 1.0 + 1.5 X + 2.0 X**2 + v $, and you estimated it by OLS?

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

import numpy as np

import statsmodels.api as sm

np.random.seed(7)

mu = 0

sigma = 1

nobs = 50

X = np.linspace(1,100,nobs)

v = np.random.normal(mu, sigma, nobs)

b1 = 1

b2 = 1.5

b3 = 2

y = b1 + b2 * X + b3 * X **2 + v

#add constant

Xt = sm.add_constant(X)

#fit linear regression model

model = sm.OLS(y, Xt).fit()

model.params

The results are [-3399.35025585, 203.49862051]. Are they still close?

Now, let’s plot everything out and you will have a better idea on what happened.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

import matplotlib.pyplot as plt

#find line of best fit

a = model.params[0]

b = model.params[1]

#add points to plot

plt.scatter(X, y, color='purple')

#add line of best fit to plot

plt.plot(X, a+ b*X)

#add fitted regression equation to plot

plt.text(10, 10000, 'y = ' + '{:.3f}'.format(a) + ' + {:.3f}'.format(b) + 'x', size=12)

While the blue line is the estimated model, the TRUE $y$s are the purple dots.

This example shows that unless the mean of $y_t$ conditional on $X_t$ really is a linear function of $X_t$, the regression model in equation \refeq{eq:linear} is NOT correctly specified. Thus, the results of OLS are meaningless and misleading. We will discuss this kind of misspecification in later posts.